-

Traders return in U.K. and U.S.; China and Hong Kong closed

-

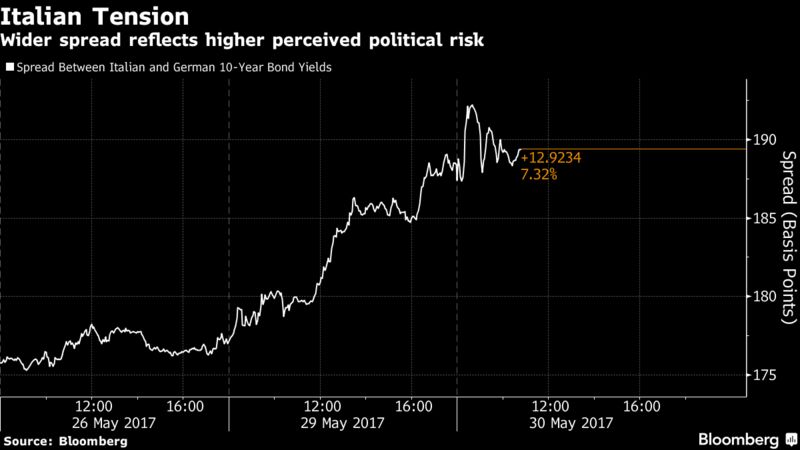

Pound edges higher; Italian assets extend drop on election

European stocks fell and the euro struggled against the dollar as investors were reminded of a few of the challenges still faced by the world’s biggest single market. Oil joined a wider selloff in commodities.

The Stoxx Europe 600 Index declined a fourth day as data showed euro-area economic confidence fell for the first time this year, and as Mario Draghi’s dovish comments to the European Parliament weighed on banking shares. A report that Greece could opt out of its next bailout payment sank to the euro, though it erased the drop after the government later issued a denial. Italian bonds edged lower as traders digest the prospect of an earlier-than-expected election.

The pullback across many assets serves as a reminder that, while equity benchmarks across the world have posted repeated records this year, potential headwinds to the global growth story remain and investor concern lingers. Elections in the U.K., Germany and Italy are looming as Brexit negotiations begin, while in the U.S. President Donald Trump’s ability to implement spending and tax-cut plans is far from certain.

Fed Bank of St. Louis President James Bullard said on Tuesday the new administration will need to fulfill the expectations that have driven the stock market higher.

“Washington does have to deliver at some point,” Bullard said in an interview on Bloomberg TV in Tokyo. “That is a concern going forward, whether the honeymoon period would end at some point and maybe the reality of American politics would settle in.”

Click here to read our Markets Live blog.

Here are some of the key events coming up:

- The euro-area’s preliminary headline inflation rate will come on Wednesday.

- Fed speakers are out and about as the FOMC’s June 13-14 meeting approaches. Lael Brainard and Robert Kaplan will be in New York on Tuesday and Wednesday, respectively.

- The U.S. jobs report Friday may bolster the case for a rate hike, with a gain of 185,000 positions expected.

- Brazil’s central-bank decision on Wednesday will probably see a cut of 75 to 100 basis points from the current 11.25 percent, according to economists.

- China’s May manufacturing PMIs on Wednesday might indicate that the nation’s 2017 growth has already peaked.

- The EIA is due to release its monthly supply reports Wednesday.

Here are the main movers in markets:

Currencies

- The euro traded little changed at $1.1167 as of 6:16 a.m. in New York. The British pound added 0.2 percent.

- The Bloomberg Dollar Spot Index was little changed.

- The yen strengthened 0.2 percent to 111.06 per dollar.

- The rand retreated 0.9 percent, extending losses for a second session after President Jacob Zuma survived a bid by some members of his party to oust him.

Stocks

- The Stoxx Europe 600 Index declined 0.2 percent.

- Futures on the S&P 500 Index fell 0.1 percent. The underlying gauge closed at a record high on Friday.

Commodities

- Gold was 0.3 percent lower at $1,264.18 an ounce.

- West Texas oil fell 0.6 percent to $49.52 per barrel; prices swung last week following the agreement by OPEC and its allies to extend cuts by nine months.

Bonds

- The yield on 10-year Treasuries declined one basis point to 2.24 percent.

- Italy’s benchmark bond yield gained one basis point after climbing seven basis points on Monday.

Asia

- Japanese stocks ended higher despite a stronger yen, with the Topix reversing earlier losses. Data showed Japan’s jobless rate stayed at the lowest in more than two decades last month, but household spending remained in a slump. Hong Kong and China markets were shut for a holiday.

by Garfield Clinton Reynolds and Samuel Potter

May 30, 2017, 8:17 PM GMT+10

Source: Bloomberg